Stagflation II

While waiting for Fitzmas, and all hell to break loose, I wanted to post this bit of economic analysis that is under the radar. I'm not an economist, but I like to play one in the blogosphere.

I visit a number of economics and stock market blogs. The state of our economy, like so many other elements of society turning to shit under Bushco, bears close scrutiny. Particularly until we have adults in charge again.

BTW, if you only want the bottom line without reading all the economic detail, scroll down to the bottom of the post.

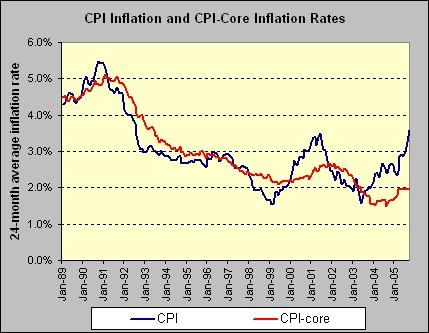

As some of you may remember, there's a continuing debate in the economics world between the those who advocate measuring inflation via the "core CPI" which excludes food/energy, or measuring inflation via the overall "CPI" which includes food/energy. It turns out that it may not matter. The two measures seem to be very closely related. I ran across this very interesting chart by Kash over at Angry Bear:

One thing notable about this chart is that the overall CPI, while more volatile, still seems to be a leading indicator of the core CPI.

Kash:

So in short, let me suggest the following: perhaps the only reason that the core rate hasn't risen more is because we haven't waited long enough. If the core rate follows the pattern of the past 15-20 years, Ben Bernanke could have his hands full, with a core rate that will be creeping upward in early 2006, just as the economy may be slowing.So if Kash is correct and history repeats itself, we're in for an extended period of increasing prices. Just how much is a good question. But let me suggest that the above chart is a period of very stable oil prices, even during the core CPI increase in 2000-02. OPEC did a great job of managing to keep oil prices between $20 and $30 per barrel pretty consistently.

Oil is currently trading down somewhat below it's September high of $70+/barrel, in the high $50's (still twice the previous levels). Unfortunately, it looks like the recent drop in oil prices is the result of an increase in oil stocks, which is occuring because of a lack of refining capacity due to Katrina. In short, the current price depression is likely artificial and short term providing the economy continues at the current pace. Just a short 12-18 months ago, $50/barrel oil would have been obscene. Now we see it as low.

Then in my blog travels I ran across a very interesting, in an economics sorta way, article by Bill Gross. For those unfamiliar with Gross, he's manages the largest bond portoflio in the world. He's highly respected for his perspectives on the economy and interest rates. In his article, he carefully builds the case that the current economic expansion is built on the housing boom. He sites the following cycle that is inevitable during any boom of this type:

1.) Housing prices will cool/stop going up very much/even go down in some cities, WHEN...Bill then goes on to show with this little chart how home equity has grown, and how the U.S. consumer has, indeed, used the increased equity as an ATM:

a. Interest rates rise to a high enough level to make the purchase of a new home a burden instead of a boon for first time buyers.

b. Mild regulatory pressure begins to reduce the amount of funny-money lending.

c. Speculators sniff the beginning of the end.

2) Home equitization should retreat shortly thereafter.

3) Consumption/the U.S. economy will then weaken when the house ATM starts running out of fresh new $25,000/$50,000/$100,000 home equity loan dollar bills.

4) The Fed will cut interest rates in order to start the game all over again.

Let me state categorically that the above sequence is barely questionable, almost inevitable, 99% unavoidable, and in modern parlance - “slam-dunk.”

Gross:

Gross:Greenspan states that homeowners borrowed $600 billion last year against the growing equity in their homes made possible by the annual gains in housing prices of near double-digits in recent years. That $600 billion amounts to nearly 7% of disposable personal income.Please note. The above chart is not refinancing. It's borrowing against equity. Assuming a rate of spending of 50% of borrowed money is very generous. Do you know anyone who borrowed against their home to save? If this statement is true, approximately one-third of the U.S GDP has been made up of home equity spending.

...

People don’t borrow money to deposit it in the bank. They borrow money to spend. If so, and using a conservative 50% figure, the chart points out that home equitization has added ½ to 1% annually to the U.S. GDP growth rate in recent years.

Wow!

Having made the case that there is a home equity boom/bust cycle that is inevitable, then making the case that the recent cycle has been a biggie, Bill then postulates this:

How weak the U.S. economy gets will depend on numerous factors: oil/natural gas prices, China’s continuing growth miracle, and of course the level of U.S. interest rates - themselves a function of the Fed and foreign willingness to buy our Treasury and corporate bonds.Well, let's see. Energy prices on the rise and likely to stay high. China's growth miracle is dependent on our consuming. And, as per the inflation argument above, the Fed increasing rates to counter inflation. Sounds like a house of cards with headwinds.

Gross:

But make no mistake about it, the froth in the U.S. housing market is about to lose its effervescence; the bubble is about to become less bubbly. If real housing prices decline in the U.S. in 2006 or 2007, a recession is nearly inevitable. If higher yields [higher interest rates] simply slow the pace of appreciation to a more rational single digit number, then we could escape with a 1-2% GDP economy.Gross predicts a best case scenario of a dramatic slowdown to 1-2% growth.....pretty anemic. This assessment is consistent with what I'm reading virtually everywhere.

So to summarize to this point. Kash sees leading indicators of inflation rising, which generally means the Fed will be increasing interest rates to slow growth and keep inflation in control. But Bill Gross is seeing a slowing economy and is predicting the Fed will decrease interest rates in 2006.

I think they're both right...Kash on inflation and Gross on GDP.

If so, the new Fed chairman Bernanke is in for a hell of a time because it's pretty difficult to raise rates and decrease them at the same time.

I've been making the case for a future period of stagflation. If you look at the above elements put together, you see precisely that phenomena. And the reason is oil.

The long term trend of the price of oil is being affected by growing international demand and the reality of peak oil. Short term American supply and demand are becoming less of a factor in oil pricing, meaning that energy prices become more independent of the American economy. Yet, because of past policies....or lack of policies...oil remains a very important part of our economy. As oil depletes without relief in demand, prices go up. As prices go up, so do prices throughout the economy.....regardless of growth/recession. Sure, there may be brief periods of energy price decline such as we're seeing today. But again I point out that $50/barrel oil was considered very high a short time ago.

Yeah yeah. I know. Greenspan keeps saying that energy price fluctuations are not nearly the factor they were in the 1970's. Perhaps. The Oil Drum has been running a series that suggests otherwise. But even if Greenspan is correct, he still admits it's two-thirds as important as it was.....still a pretty big deal. And it's important to note that during Greenspans now waning tenure, oil prices were in that OPEC controlled price rut of $20 to $30/barrel. This price stability (as opposed to absolute price) made it pretty easy for him to dismiss energy as an important factor in the economy. Compare Greenspan's tenure to this chart:

Click Image for Larger View

Click Image for Larger ViewBottom Line: I think the above makes the case for the next two years to be times of higher energy prices, moderate to high inflation, lower home prices, lower consumer spending, and a recession. Personally I'd call it a period of stagflation with increasing prices and increasing unemployment. And while some growth may return with lowering interest rates (which Bill Gross is predicting in 2006), it will only fuel inflation (which Kash is predicting). Get ready for inflation to be a part of your daily life.

And who do we have to thank? Mostly BushCo. But Democrats have also been sitting on their hands through this economically destructive period of excessive government spending, chronic economic drag resulting in low interest rates created by the Iraq war and fear of terrorists, and zero in the way of an innovative energy policy. We can only hope that future administrations and Congress's will get with it and spur energy innovations that move our economy away from being petroleum based. Until then, more dramatic rising prices will be a fact of life.

posted by greyhair @ 2:39 PM

1 comments

![]()

![]()

1 Comments:

This all makes my head hurt.

For the past two years I've been expecting a depression. As in the Great Depression. I'm still not convinced it isn't going to happen.

Actually it is already happening for so many Americans, especially the people who will be trapped in Bushvilles

"...and spur energy innovations that move our economy away from being petroleum based..."

I'm holding my breath on this one.

Post a Comment

<< Home